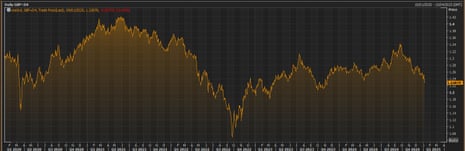

Pound falls below $1.23 to 14-month low

The pound has dropped to a 14-month low in early trading in London, as the bond-market sell-off fuels anxiety over UK assets.

Sterling has lost a cent against the US dollar, extending its recent losses, falling to around $1.226.

That’s its lowest level since November 2023, suggesting that the jump in UK borrowing costs this week is continuing to worry the markets, at a time when the dollar is generally strengthening.

Michael Brown, senior research strategist at brokerage Pepperstone, has warned that “things are also getting rather ugly” in the UK.

Brown told clients this morning:

This dynamic, of yields moving higher, as the respective currency falls, is a classic sign of fiscal de-anchoring taking place, and of participants losing confidence in the Government in question’s ability to exert control over the fiscal backdrop.

We’re not at the Truss/Kwarteng stage just yet, but things are clearly on very shaky ground indeed.

Brown added that his preference is to be ‘short GBP’ – ie, betting that the currency will continue to fall.

Despite recent losses, the pound is still comfortably above the record low hit after the 2022 mini-budget, when it plunged to near-parity against the US dollar.

Key events Show key events only Please turn on JavaScript to use this feature

Richard Partington

One City analyst said last night the Treasury’s unusual step to comment on the bond market could be being taken by hedge fund investors as “the scent of blood in the water” as Reeves battles to maintain authority.

Brad Bechtel, global head of foreign exchange at Jefferies, said the sell-off in the pound showed the UK was seeing a “micro version” of the bond market meltdown witnessed after Liz Truss’s 2022 mini budget.

Bechtel said:

“UK gilts continue to melt down and that has so far not impacted the currency as much as it did during the Liz Truss episode, that is until today.

“The pound seems to be reacting to gilts more and more and that means we are spilling further and further into fiscal emergency territory.”

“We don’t ‘feel’ like we are in the same Liz Truss zone right now, mostly because we haven’t seen an LDI blow up, but we are in a micro version of that for sure.”

However, other analysts said the comparisons with the short-lived prime minister’s tenure were overblown.

“It’s nice to talk about this as being a Truss moment. Those comparisons are easy and obvious. But we’re a long way from that,” said Mark Capleton, an analyst at Bank of America.

“Though in level terms we’re higher than then, there has since been a big global sell off, and it has been far more gradual by comparison.”

He said nine of the top 10 daily movements in the gilt market since 1992 had come during 2022. “We’re a long way from that.”

However, he added:

“Obviously people are concerned about a vicious circle with the fiscal arithmetic and the possibility that a further rise in yields could create the need for tightening measures from the chancellor in March.”

The drop in the pound may make it trickier for the Bank of England to lower interest rates as soon as hoped in 2025.

Two two quarter-point cuts to Bank Rate are priced in for this year, bringing rates down from 4.75% to 4.25% by December, but the odds on a cut as soon as February have dipped slightly this week.

Jim Reid, an analyst at Deutsche Bank, explains:

“With sterling weakening, that meant growing questions were asked about whether the Bank of England could cut rates as fast as expected.

“Indeed, investors dialled back their expectations for rate cuts this year by four and a half basis points compared to the previous day, so they now only see 48.5 basis points by the December meeting.

“So collectively, this rise in yields is adding to the risk that the Government will breach their fiscal rules and have to announce further consolidation (tax rises and/or spending cuts), whilst the weaker currency will add to inflationary pressures at the same time.”

Greggs warns lower consumer confidence is hitting sales

Baking chain Greggs has warned that it faces ‘headwinds’ as UK consumer confidence falls, in a fresh blow to the economic outlook.

Greggs reported that sales growth slowed at the end of last year. In the final quarter of 2024, sales at its company-managed shops rose by 2.5%, weaker than the full-year sales growth of 5.5%.

Greggs says that it faced a “more challenging market backdrop” in the second half of 2024, as weaker consumer confidence hits footfall on the high street, meaning fewer visits to its stores.

Chief executive Roisin Currie says:

Whilst lower consumer confidence continues to impact High Street footfall and expenditure, our value-for-money offer and the quality of our freshly-prepared food and drink position us well to meet the headwinds we expect to see in the year ahead, and we remain confident in the significant long-term opportunity for growth.”

Shares in Greggs have fallen by 9.5% this morning.

Tesco and M&S shares fall despite strong Christmas trading

A flurry of top UK retailers are revealing how they performed over the crucial Christmas period – and seeing their shares fall.

Tesco, the UK’s largest supermarket, declared it enjoyed its “biggest ever Christmas”, with sales at established UK stores rising by 4% in the six weeks to 4 January. But shares have dropped by 1.6% this morning.

Marks & Spencer says it also had a good Christmas, with like-for-like food sales up 8.9% in the 13 weeks to 28 December.

M&S warns, though that “the external environment remains challenging, with cost and economic headwinds to navigate”. Its shares have fallen by 6% this morning.

Discount retailer B&M reported a 2.8% increase in UK sales in the last quarter of 2024, with CEO Alex Russo saying “the business remains undistracted by the current economic headlines”.

B&M has also narrowed its forecast for profit growth this year, knocking its shares down by 10% this morning.

Bond panic makes the front pages

The bond market mayhem makes the front pages of several UK newspapers today.

The Daily Telegraph splashed on last night’s statement from the Treasury that they have an ‘iron grip’ on the public finances, calling it an intervention designed to stabilise the markets:

The Daily Mail says the rise in borrowing costs is a ‘red alert’ warning for chancellor Reeves, who may have to cut spending or lift taxes to keep within her fiscal rules.

The i picks up on that point too, saying Britain’s borrowing costs have turned ‘toxic’.

🚨

Another bumpy day in markets beckons.

UK govt bond yields jump up again to fresh highs (chart 1).

Pound weaker against dollar (chart 2).

Not great. pic.twitter.com/nM7ZxwPwo3

UK bond sell-off continues

UK borrowing costs are rising again this morning, despite the government’s efforts to calm the markets last night.

The yield, or interest rate, on benchmark 10-year UK debt rose by 12 basis points (or 0.12 percentage points) in early trading in London to 4.921%, the highest since 2008.

Thirty-year bond yields, which hit 28-year highs this week, are rising again too – up over 10 basis points to 5.474%.

These moves suggest investors are still fretting about the outlook for the UK economy, given concerns about low growth and inflationary pressures.

It also shows the Treasury’s insistence last night that they have an ‘iron grip’ on the public finances has not eased the pressure….

Britain’s bond turmoil invokes memory of 1976 debt crisis

Former Bank of England policymaker Martin Weale has suggested that we should look to 1976, rather than 2022, for a comparison with the current market anxiety.

1976 was an infamous year in UK economic history, when a plunge in the value of the pound forced the Labour government to turn to the International Monetary Fund for a bailout, with strict spending cuts attached.

Weale has told Bloomberg that this week’s rise in borrowing costs and fall in the value of sterling echo the 1976 debt crisis “nightmare”.

Weale, a professor of economics at King’s College London, says:

“We haven’t really seen the toxic combination of a sharp fall in sterling and long-term interest rates going up since 1976. That led to the IMF bailout.

So far we are not in that position but it must be one of the chancellor’s nightmares.”

The 1976 crisis was highly dramatic; chancellor Denis Healey was forced to abandon a flight to the IMF’s September 1976 meeting in Manila, to return to the Labour party conference in Blackpool and deliver a memorable speech defending his planned spending cuts as negotiations began with the Fund over the the bailout.

Rachel Reeves heading to China this week to build bridges

The pound’s tumble comes as Rachel Reeves prepares to fly to China in a bid to build closer ties with Beijing.

The chancellor, who is travelling with a delegation of City bigwigs, is holding the visit as part of a concerted effort to build bridges with China, as part of the government’s push for growth.

Our economics editor Heather Stewart explains:

City businesses have urged Reeves to help ensure China is not placed on the higher, more stringent, tier of a new “foreign influence registration scheme” – a decision ultimately to be made by the Home Office.

Lobbyists for overseas governments will have to declare their role under this new regime, but the “enhanced” tier will force companies carrying out any activity on behalf of another state to make themselves known – something business groups fear could prevent closer ties.

The chancellor will take the Bank of England governor, Andrew Bailey, with her on the visit to Beijing and Shanghai, as well as the FCA chief executive, Nikhil Rathi, and a string of senior banking figures, including HSBC’s chair, Mark Tucker.

Reeves will meet China’s vice-premier, He Lifeng, in Beijing before flying to Shanghai for discussions with UK firms operating in China.

Enhanced cooperation on financial services is at the heart of the Treasury’s hopes for the trip. Reeves lavished praise on the sector in her Mansion House speech last year, calling it the “crown jewel” of the UK economy.

Pound falls below $1.23 to 14-month low

The pound has dropped to a 14-month low in early trading in London, as the bond-market sell-off fuels anxiety over UK assets.

Sterling has lost a cent against the US dollar, extending its recent losses, falling to around $1.226.

That’s its lowest level since November 2023, suggesting that the jump in UK borrowing costs this week is continuing to worry the markets, at a time when the dollar is generally strengthening.

Michael Brown, senior research strategist at brokerage Pepperstone, has warned that “things are also getting rather ugly” in the UK.

Brown told clients this morning:

This dynamic, of yields moving higher, as the respective currency falls, is a classic sign of fiscal de-anchoring taking place, and of participants losing confidence in the Government in question’s ability to exert control over the fiscal backdrop.

We’re not at the Truss/Kwarteng stage just yet, but things are clearly on very shaky ground indeed.

Brown added that his preference is to be ‘short GBP’ – ie, betting that the currency will continue to fall.

Despite recent losses, the pound is still comfortably above the record low hit after the 2022 mini-budget, when it plunged to near-parity against the US dollar.

Introduction: UK bond sell-off fuels fears of another Truss moment

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

After two days of sharp rises in UK borrowing, City experts are harking back to previous episodes of financial panic – including the dark days after Liz Truss’s mini-budget of 2022.

Britain finds itself in the eye of a global bond market storm at the moment, with the pound also weakening. Yesterday, the yield (rate of return) on 10-year UK government debt hit its highest since the 2008 financial crisis, a day after the 30-year bond yield hit its highest level since 1998.

Last night, Rachel Reeves insisted she had an ‘iron grip’ on the nation’s finances, with a Treasury spokesperson declaring:

“No one should be under any doubt that meeting the fiscal rules is non-negotiable and the Government will have an iron grip on the public finances.

“UK debt is the second lowest in the G7 and only the OBR’s forecast can accurately predict how much headroom the government has - anything else is pure speculation.

“Kick-starting economic growth is the number one mission of this Government as we deliver on our Plan for Change. Over the coming weeks and months, the Chancellor will leave no stone unturned in her determination to deliver economic growth and fight for working people.”

It’s not exactly ‘pure speculation’, though, to point out that rising bond yields eat into the relatively small headroom available to the chancellor to hit her fiscal rules (to not borrow to fund day-to-day spending, and to show debt falling in five year’s time).

If the headroom has vanished by the spring statement in March, it will leave the chancellor with an unpalatable choice – cut government spending, despite demands from the public and cabinet colleagues for better services, or raise taxes further.

The borrowing costs of other governments have also been rising in recent sessions, inculding the US, where there are fears that Donald Trump’s presidency will drive up inflation, making interest rate cuts less likely.

But the situation in the UK feels more acute.

Ipek Ozkardeskaya, senior analyst at Swissquote Bank, says “the UK’s demons are back”, driven by heightened fiscal concerns – which are “evoking memories of Liz Truss’s chaotic ‘mini-budget days.’”

Ozkardeskaya added:

Back then, markets lost confidence in the government’s spending plans, triggering an aggressive selloff that forced the BoE to intervene. The fallout toppled Truss’s government, setting the stage for Labour’s strong electoral win.

But now, the newly elected Labour government, which promised to rescue the country, improve finances, and boost growth, faces its own reckoning. To deliver on its ambitions, it needs market support – a resource proving elusive. Without it, borrowing costs will spiral higher, forcing tougher choices: more taxes, less spending, and weaker growth. And none of that bodes well for the pound.

The sell-off in 2022, after chancellor Kwasi Kwarteng delivered a budget of unfunded tax cuts, was certainly more aggressive than what we’ve seen this week. But long-term borrowing costs are now higher than in the Truss panic.

Kyle Rodda, senior financial market analyst at Capital.com, fears the tumble in UK asset prices could be a sign of another “simmering financial crisis”:

There’s a mini-crisis brewing in UK markets amidst a broad-based sell-off in the country’s assets. For no explicable reason aside from already known factors like weak growth, elevated inflation, and unsustainable fiscal settings, stocks, bonds and the Pound plunged, in moves reminiscent of the 2022 Truss meltdown.

The moves indicate a looming crisis of confidence in the UK and reflects expectations of ongoing and long-term economic malaise which will only be addressed by massive reform.

Dutch bank ING say that several factors are pushing up UK bond yields, including Labour’s spending ambitions, sticky inflation, higher US rates and supply pressures.

But in cheering news for the Treasury, IN’s senior european rates strategist Michiel Tukker is confident that we’re not facing a “sovereign crisis”.

Tukker told clients:

It’s important to note that the demand from foreign buyers remains strong, which reduces the repeat risks of a Liz Truss moment. So whilst rates can stay higher, we don’t expect any steep sell-offs on the back of sovereign risk.

Also, keep in mind that the Truss turmoil was exaggerated by a liquidity crunch among pension funds due to interest rate hedges suddenly moving against them. This time the move up is more gradual, which should prevent such a spiral higher in gilt yields.

The agenda

-

10am GMT: Eurozone retail sales for November

-

12.30pm GMT: Challenger survey of US job cuts in December

-

4pm GMT: Bank of England policymaker Sarah Breeden gives speech