Dollar hits three-year low as Trump's attacks on Powell worry investors

Good morning, and welcome to our rolling coverage of business, the financial markets, and the world economy.

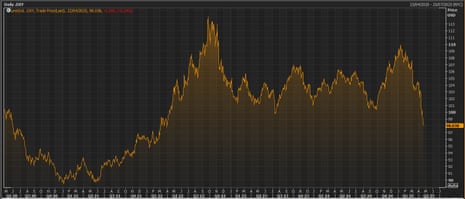

The US dollar has sunk to a three-year low as the exodus from US assets gathers pace.

Traders are anxious after Donald Trump launched another blistering attack on America’s top central banker yesterday, calling Jerome Powell “Mr. Too Late” and “a major loser”, as the US president intensified his calls for US interest rate cuts.

This has pushed the dollar down against a basket of currencies to its lowest level since March 2022.

Against the yen, the dollar has hit a seven month low, trading at ¥140 for the first time since last September.

Last week, Trump posted that “Powell’s termination cannot come fast enough”.

Tony Sycamore, market analyst at IG, says Trump’s attacks on Powell are leading to a lack of confidence in the markets:

Their relationship has long been contentious. Despite appointing Powell in 2017, Trump has since expressed regret, criticising Powell for “bad decisions” and being “always too late and wrong.”

Powell has countered by warning that Trump’s tariffs could spur higher inflation and slower growth, contradicting Trump’s claims of his policies’ economic benefits.

Yesterday (when European markets were closed), there were further losses on Wall Street, where the Dow Jones Industrial Average lost another 2.5%, or almost 1,000 points.

Investors are also disappointed at the lack of progress in trade talks, following the hefty tariffs announced by Trump earlier this month.

This is creating a worrying situation, in which the dollar, the US stock markets and US government bond prices are all falling. Typically in a crisis, US government debt and the dollar would rally as traders sought out a safe haven.

“The market reaction is arguably more about broader investor concerns that less credible US policy-making may erode the exorbitant privilege that has allowed the US to run high twin deficits than it is about the specific risk of political influence over the Fed’s rates policy,” explains Jim Reid, market strategist at Deutsche Bank.

The International Monetary Fund (IMF) will give its verdict on the economic consequences of the US trade war later today, when it releases the latest forecasts in its World Economic Outlook.

Central bank governors, finance ministers, and other economic leaders are heading to Washington for the annual IMF-World Bank Spring Meetings.

The agenda

-

9am BST: ECB Survey of Professional Forecasters

-

2pm BST: International Monetary Fund releases its latest World Economic Outlook.

-

3pm BST: European Union Consumer Confidence report

-

3.15pm: IMF releases its Global Financial Stability Report

Key events Show key events only Please turn on JavaScript to use this feature

Gold hits $3,500 for first time

Worried investors are continuing to pile into gold, pushing it up to fresh record highs today.

Gold hit $3,500 per ounce for the first time this morning, extending a monster rally that has pushed bullion up from $2,623/ounce at the start of this year.

Matt Britzman, senior equity analyst at Hargreaves Lansdown, says:

The tariff tug-of-war still has no end in sight, and now the Powell power struggle is adding more fuel to the fire, with whispers from the White House about his potential ousting rattling already jittery investors. At this rate, even bad news might be seen as a buying signal - if only because something, anything, from Washington might offer a sliver of direction.

Markets are now itching for real progress on trade deals - posts from the President on Truth Social or X just aren’t cutting the mustard anymore. Investors want ink on paper, not just words, as a clear signal that movement is happening - and the clock is ticking.

This lack of certainty is sending investors right into the arms of traditional safe haven assets, with gold and the Japanese yen both cashing in on the drama.

US imposes tariffs up to 3,521% on Southeast Asia solar imports

Overnight, the US has announced plans to impose hefty new tariffs on imports of solar panels from four South East Asian countries.

The move follows an anti-dumping investigation, and means crystalline photovoltaic cells sold to the US will incur painful new trade levies.

Cambodia is hardest hit, with a new tariff of above 3,000% on its solar panels.

Bloomberg reports:

The US imported $12.9 billion in solar equipment last year from the four countries that would be subject to the new duties, according to BloombergNEF. That represents about 77% of total module imports.

Companies not named in Vietnam face duties of as much as 395.9% with Thailand set at 375.2%. Country-wide rates for Malaysia were posted at 34.4%.

Jinko Solar was assessed duties of about 245% for exports from Vietnam and 40% for exports from Malaysia. Trina Solar in Thailand faces levies of 375% and more than 200% from Vietnam. JA Solar modules from Vietnam could be assessed at about 120%.

The new tariffs follow an investigation by the U.S. Department of Commerce into claims by American producers that Chinese companies in those countries were dumping solar cells and panels in the U.S. at artificially low prices.

Thailand says talks with US over Trump tariff plan delayed

Earlier today, Thailand revaled that talks with the US over tariffs have been postponed.

Thai-U.S. trade negotiations have been scheduled to take place tomorrow (April 23). But Thailand, which is seeking a reprieve from Trump administration’s plan to levy a 36% tariff on its goods, has said ministerial level talks have been delayed.

Prime minister Paetongtarn Shinawatra has said the schedule for talks has been adjusted because the US has asked Bangkok to review important issues.

Paetongtarn said that Thai agriculture exports and additional imports were being examined, and insisted:

“We’re not too slow and we are reviewing issues, including our tariffs that may be adjusted appropriately.

“We are consulting academics and all parties and doing our best in this situation.

“We are protecting the agricultural interests as much as possible.”

Bloomberg: Japan’s Kato aims to further FX dialogue with Bessent this week

Japan’s Minister of Finance Katsunobu Kato said today he aims to build on close discussions pertaining to currencies when he meets his US counterpart Scott Bessent in Washington this week, Bloomberg reports.

Kato told a press conference today:

“Treasury Secretary Bessent and I are in close contact on currencies, and I would like to take this opportunity to hold further discussions during my visit.

Kato was scheduled to depart for Washington today, where he’ll represent Japan at a series of meetings including Group of 20 and International Monetary Fund gatherings. He said the timing for a meeting with Bessent is still under discussion.

Pound at seven-month high

The weakness of the dollar has pushed the pound up to its highest level against the US currency in seven months.

Sterling climbed to $1.3423 in early trading, up around half a cent, to its highest level since last September.

Reeves to make case for free global trade at Washington IMF talks

Pippa Crerar

Rachel Reeves will fly to Washington this week to argue for global free trade in the face of Donald Trump’s punitive tariffs, amid continued international economic turbulence.

The UK chancellor will use the spring meetings of the International Monetary Fund, which is attended by top finance ministers and central bankers, to make the case that free trade is in both British and global interests.

One senior official said:

“We’re facing a new economic reality, but we’re a heavily trading country, with the value of our exports the equivalent of 60% of GDP, so it’s always in our own interests to promote free trade.”

Reeves will urge the Trump administration to cut punitive tariffs on UK car and steel exports and step up negotiations for a trade deal when she meets the US Treasury secretary, Scott Bessent, for the first time, allies said. He is seen as one of the less hardline US voices on trade.

Dollar hits three-year low as Trump's attacks on Powell worry investors

Good morning, and welcome to our rolling coverage of business, the financial markets, and the world economy.

The US dollar has sunk to a three-year low as the exodus from US assets gathers pace.

Traders are anxious after Donald Trump launched another blistering attack on America’s top central banker yesterday, calling Jerome Powell “Mr. Too Late” and “a major loser”, as the US president intensified his calls for US interest rate cuts.

This has pushed the dollar down against a basket of currencies to its lowest level since March 2022.

Against the yen, the dollar has hit a seven month low, trading at ¥140 for the first time since last September.

Last week, Trump posted that “Powell’s termination cannot come fast enough”.

Tony Sycamore, market analyst at IG, says Trump’s attacks on Powell are leading to a lack of confidence in the markets:

Their relationship has long been contentious. Despite appointing Powell in 2017, Trump has since expressed regret, criticising Powell for “bad decisions” and being “always too late and wrong.”

Powell has countered by warning that Trump’s tariffs could spur higher inflation and slower growth, contradicting Trump’s claims of his policies’ economic benefits.

Yesterday (when European markets were closed), there were further losses on Wall Street, where the Dow Jones Industrial Average lost another 2.5%, or almost 1,000 points.

Investors are also disappointed at the lack of progress in trade talks, following the hefty tariffs announced by Trump earlier this month.

This is creating a worrying situation, in which the dollar, the US stock markets and US government bond prices are all falling. Typically in a crisis, US government debt and the dollar would rally as traders sought out a safe haven.

“The market reaction is arguably more about broader investor concerns that less credible US policy-making may erode the exorbitant privilege that has allowed the US to run high twin deficits than it is about the specific risk of political influence over the Fed’s rates policy,” explains Jim Reid, market strategist at Deutsche Bank.

The International Monetary Fund (IMF) will give its verdict on the economic consequences of the US trade war later today, when it releases the latest forecasts in its World Economic Outlook.

Central bank governors, finance ministers, and other economic leaders are heading to Washington for the annual IMF-World Bank Spring Meetings.

The agenda

-

9am BST: ECB Survey of Professional Forecasters

-

2pm BST: International Monetary Fund releases its latest World Economic Outlook.

-

3pm BST: European Union Consumer Confidence report

-

3.15pm: IMF releases its Global Financial Stability Report