Analyst: Oil prices could hit $100/bbl as strait of Hormuz traffic halts

Analysts are warning that the US-Israel war with Iran could drive oil prices up to $100 a barrel.

Consultancy firm Wood Mackenzie is warning that higher oil and gas prices are certain, and that oil prices could potentially exceeding $100/barrel if tanker flows through the strait of Hormuz are not quickly restored.

They say tanker traffic has been effectively halted, after Iran warned shipping away from the waterway and insurers withdrew coverage.

In the current scenario, oil prices over US$100/bbl are possible if transit flows are not re-established quickly, according to Alan Gelder, SVP of Refining, Chemicals and Oil Markets at Wood Mackenzie.

Gelder explains:

“The key question is when do vessels re-establish export flows.

“No doubt, tanker rates and insurance will increase dramatically, but these costs would only be a small part of the oil price impact associated with a curtailment of oil flows if they last for more than a few days.”

Even in the optimistic scenario where Iran cooperates with the US, it could take a few weeks for export flows to re-establish themselves, Gelder added, saying:

“During that time, oil prices are heavily risked to the upside.

The most recent comparison is during the early days of the Russia/Ukraine conflict, when the fear of loss of Russian supplies drove the oil price to over US$125/bbl.”

Brent crude last traded as high as $100/barrel in 2022, early in the Russia-Ukraine war.

Key events Show key events only Please turn on JavaScript to use this feature

Surging European gas prices

European gas prices have soared, as Qatar’s decision to shut down liquefied natural gas production (see earlier post) raises fears of shortages.

The Dutch day-ahead gas contract is up 39% today at €44.5 per megawatt hour (MWh), up from €32 per megawatt hour (MWh) on Friday.

That’s still lower than in the early months of the Ukraine war, though (it hit €337MWh in August 2022).

Chris Beauchamp, chief market analyst at IG, says:

“The huge bounce in European natural gas prices threatens to upset the more positive outlook for UK inflation and consumer spending.

Hopes that pricing pressures would ease and consumers could spend more could be dashed as a price spike similar to 2022 causes a major headache for both policymakers and consumers, potentially disrupting the plan for more UK rate cuts.”

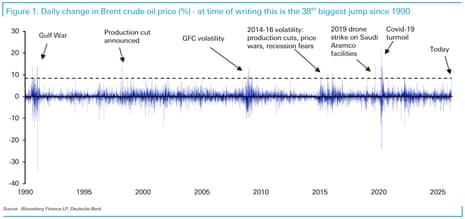

Deutsche Bank: “Only” the 38th largest oil spike since 1990

A little earlier today, Brent crude was up 8.4% this session.

Although that’s a sharp move, it’s only the 38th biggest daily gain over the last 36 years, according to Deutsche Bank market strategist Jim Reid.

He explains:

So even though it’s a big move, to get into the top 20, 10 and 5 it would need to be up +9.6%, +13.6% and +13.9% respectively. There were huge moves around the GFC [Great Financial Crisis] and Covid-19 turmoil, whilst the Gulf War in 1990-91 also saw several double-digit gains.

Going forward, much will depend on the Strait of Hormuz. It seems it’s not officially closed but passage through it would be hazardous at the moment with self-imposed restrictions from virtually all that normally travel through it.

Gold, silver and aluminium prices follow oil higher

Phillip Inman

Investors are closely watching developments around shipping in the Strait of Hormuz, an important commodities trade route disrupted by Iranian attacks on US military bases in the region.

Most of the concern in Europe, China, India and Japan relates to the transport of oil and liquid natural gas (LNG) as US and Israeli strikes in Iran fuel concerns about prolonged conflict in the Middle East.

Industrial metals prices tend to be slower to react to global events.

Nevertheless, aluminium prices rose to their highest in more than a month on concerns that the region, a major producer of the metal, will suffer from a prolonged war.

The benchmark aluminium price on the London Metal Exchange was up 3.1% at $3,236 a metric ton at 10.50am after touching $3,254 for its highest since January 29.

Neil Welsh at Britannia Global Markets, said.

“Base metals are largely higher this morning as aluminium climbs on concerns that a critical supply route for Middle Eastern producers will be disrupted by conflict in a region responsible for a significant chunk of global output.

“The region accounts for about 9% of the world’s aluminium production capacity and prices have typically been sensitive to spikes in regional tensions.”

Increases in metals prices are expected to reverse should the war become protracted and result in a rise in energy prices that in turn hit global growth.

“We should expect global investment sentiment to falter, undermining industrial metals demand growth - including copper,” said Panmure Liberum analyst Tom Price.

Copper nudged higher at 0.2% to $13,370 a ton, zinc gained 1% to $3,351, lead rose 0.6% to $1,974 and tin lost 1.1% to $57,105. Nickel retreated by 1.1% to $17,645.

Of the metals, gold is almost purely sentiment driven and the best indicator of investor worries.

“Gold is the sum of all fears,” said Ross Norman, the chief executive of Metals Daily

“But is also a very small lifeboat, which means the price soars in times like these.”

The gold price was up 3% in early trading to £5,405.90 , which Norman said was an indication traders view the curent conflict in the middle east as a “strong, but limited event so far.”

“Gold is a safe haven asset, but there is a caveat to today’s rise, which is that event-driven rallies rarely last,” said Norman.

Silver prices on international markets also increased, though by a more muted 1.7% at $95.36 per ounce.

QatarEnergy halts LNG production due to attacks

QatarEnergy, the country’s state-owned petroleum company, has halted production of liquefied natural gas (LNG) and associated products at two sites.

The shutdown is due to military attacks on facilities in Ras Laffan (north of Doha) and Mesaieed (south of Doha), it says.

VIX fear index hits highest since November

Wall Street’s ‘fear index’ has hit its highest level in three months.

The VIX index, which tracks volatility in the markets, is up 16% so far today, to its highest level since November 2025.

Lukman Otunuga, senior market analyst at global broker FXTM, says:

“The Iran crisis has entered a dangerous new phase, and markets are reacting accordingly. With oil surging, volatility spiking and investors rushing into traditional safe havens, we could see heightened turbulence over the coming days and weeks. Much will depend on whether diplomatic channels reopen quickly, but for now, risk sentiment remains fragile.”

Shippers are once again avoiding the Suez Canal, Bloomberg report, as the US- Israel war with Iran dashed hopes of an imminent revival for the key global trade route.

A.P. Moller-Maersk, Hapag-Lloyd and France’s CMA CGM have all said they’re suspending passage or routing services away from Suez, reflecting fears that Iranian-backed Yemeni rebels might resume attacks on vessels in the southern Red Sea.

If the oil price hits $100 a barrel, or more, it would push up inflation and weaken growth.

According to Maurizio Carulli, global energy analyst at Quilter Cheviot, a $10/barrel change in the oil price can add 30-40 basis points (0.03 to 0.04 percentage point) to consumer inflation indexes, and shave off 10-30 basis points from global GDP growth.

Today, Brent crude has gained $5.50 to $78.42 per barrel.

Carulli says:

“Oil supply and demand fundamentals until Friday had pointed at a surplus in 2026, however, that is quickly changing as events in the Middle East play out. Recent weeks had seen the oil price rise from $60/bbl at the beginning of January to $72/bbl on Friday, with it climbing further today to $80/bbl as markets factor in the increased geopolitical risk.

“Depending on how, and for how long, the current military action will continue, the oil price will adjust quite quickly. So, if the situation will calm down over the next few weeks, as it is well possible, the price is likely to revert to $60-65/bbl, given oil production is in excess of demand, and Opec+ has some spare capacity to increase production further. And, vice versa, if the situation precipitates into a wide-spread and prolonged Middle East war, with shipping across the Strait of Hormuz halted, then the oil price could feasibly rise to $100/bbl and above.”

Christian Schulz, chief economist at AllianzGI, says markets face a significant – but not yet destabilising – shock after the US and Israel launched strikes against Iranian military targets.

Much depends on whether the conflict spills into broader regional or domestic instability, Schulz says, adding:

-

US and Israeli airstrikes and Iranian attacks in retaliation have raised the risk of a full-scale Middle East war

-

The death of Iran’s supreme leader raises the chances of regime change along with protracted instability in Iran and may reduce the risk of a sustained regional conflict.

-

Markets will likely demand a higher premium, at least temporarily, until clarity emerges on Iran’s internal stability and the intentions of its geopolitical partners.

-

We think oil prices will likely rise even if a sustained closure of the Strait of Hormuz remains unlikely for now; in broader financial markets, US Treasuries, the US dollar and gold may gain, while equities may see a sharp but potentially short‑lived sell-off.

RAC: How higher oil prices could hit drivers

RAC head of policy Simon Williams has crunched the impact on higher oil prices at petrol and diesel pumps:

“While the conflict in the Middle East undoubtedly has the potential to push up pump prices in the UK, it’s not a certainty. The oil price would have to rise significantly and stay that way for some time to have a dramatic effect.

“Forecourt prices were already on the rise due oil trading nearer to $70 a barrel in the last few weeks. Regardless of the current situation, petrol rose by a penny a litre in February and is likely to go up by another penny in the next week or so to an average of 134p a litre.

“If oil were to climb to and stay at the $80 a barrel mark, then drivers could expect to pay an average of 136p for petrol. At $90, we’d be looking at over 140p a litre and $100 would take us nearer to 150p, but it’s all too soon to know.”

The losses in London, Frankfurt, Paris, Milan and Madrid today have pulled the pan-European Stoxx 600 share index down to a two week low.

The Stoxx 600 is down 1.4% so far today, at 624.94 points, falling away from the record highs seen last week.

The eurozone is the major economy that is most exposed to the Iran crisis, Dutch bank ING says.

In a new research note, ING explain that military action in the Middle East could have significant implications for the global economy and markets.

Those “macro consequences” will hit hardest in Europe, where the timing could not be worse.

They write:

The eurozone was finally emerging from its long period of stagnation, with tentative green shoots of recovery emerging – though recently, these have been undermined by new uncertainty regarding tariffs. Now the region could face an energy shock on top of a trade shock.

Europe imports essentially all of its oil and a significant share of its LNG. A surge in energy prices and potentially even energy supply disruption could bring back memories of the energy cost crisis from late 2021 to 2023. There are currently two important differences compared with the situation back then: Europe doesn’t have to ‘derisk’ from a single important energy provider; and the oil price crisis comes at the end of the winter, not the start.

This puts the European Central Bank in “a genuine dilemma”, ING add:

Services inflation is still sticky, and an oil shock would push headline inflation higher – yet the growth outlook is simultaneously deteriorating under the combined weight of tariffs, uncertainty, and now energy costs. Back in December, an ECB analysis showed that a 14% increase in oil prices would push up inflation by 0.5ppt and could reduce GDP growth by 0.1ppt.

However, this would only be the price effect, not the supply chain disruption effect. Given the still relatively fresh memories of the recent inflation surge, the ECB is unlikely to see any new oil price-driven inflation spike as transitory or even deflationary. However, to see a rate hike, the eurozone economy would have to show clear resilience.

Benchmark European diesel refining margins rose nearly 25% on Monday, to their widest since November 20, as the U.S.-Iran conflict disrupted supplies in the Middle East, Reuters reports.

Margins traded at $30.75 a barrel this morning, up by nearly $6, after hitting a session high of $33.76 earlier.

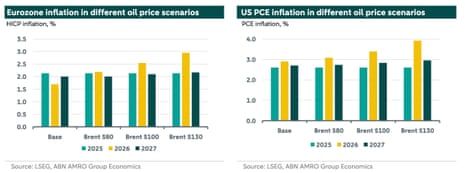

Analysts at ABN Amro predict that the rise in the oil price will have a bigger impact on inflation rather than growth.

They have drawn up three inflation scenarios, covering Brent crude at $80/barrel (roughly its current level), $100 and $130 per barrel.

In the latter scenario, US inflation approaches 4% this year – double the Federal Reserve’s target.

ABN Amro say:

Already facing above target inflation, higher oil prices put the Fed in an even more difficult situation. Headline inflation will rise substantially, while core inflation, which excludes energy prices, barely moves. The usual policy response, which remainsthe most likely for now, is therefore to look through the oil price shock, seeing as it’s a one-off inflationary impulse.

In the current setting, things are more complicated, because the scenario of oversupply with falling energy prices provided a tailwind in headline inflation, which could be used to argue in favour of rate cuts. Higher energy prices, and a resurgence of inflation,could very well tilt the already fragile balance in the FOMC towards holding rates, on the fear of inflation expectations becoming de-anchored, even if the shock is temporary. For our base case to alter, we would need to see, or expect, sustained higher oil prices. Signs of inflation de-anchoring would put a nail in the coffin for rate cuts this year.

Turning to the eurozone, in the mildest scenario(Brent $80), inflation goes from being well below the ECB’s 2%target to moving broadlyback to target and staying there. Even in the mostsevere (Brent $130) scenario, while eurozone inflation is boosted by1.3pp in 2026, the lasting impact is relatively mild, with 2027 inflation only 0.2pphigher.